Most people think they understand their IRA.

You put money in.

You wait.

You take it out when you retire.

Simple—right?

Not exactly.

An Individual Retirement Account (IRA) is far more flexible, powerful, and misunderstood than most investors realize. In fact, many people are shocked when they discover what they can do with their IRA—and even more shocked when they learn what they should never do with it.

This article breaks down the surprising truths about IRAs: what’s allowed, what’s strategic, what’s risky, and how smart investors use IRAs as long-term tools—not dusty retirement boxes.

First, What Is an IRA Really?

An IRA is not an investment.

It is a tax-advantaged container.

Inside that container, you can hold different types of investments—depending on the rules of your specific IRA and the custodian managing it.

The power of an IRA is not just what you earn.

It’s how much of it you keep after taxes.

You Can Choose How Your IRA Is Invested

Many people assume their IRA is limited to a small menu of options.

In reality, depending on your provider, an IRA can hold:

- Stocks

- Bonds

- Mutual funds

- ETFs

- Index funds

And in some cases (with special structures):

- Real estate

- Private investments

- Alternative assets

Your IRA does not decide your future.

Your investment choices do.

You Can Move and Combine IRAs (Without Penalties)

One of the most underused IRA features is portability.

You can:

- Roll over old employer retirement accounts into an IRA

- Consolidate multiple IRAs into one

- Change custodians for better fees or options

When done correctly, these moves are not taxable events.

Smart investors simplify accounts to:

- Reduce fees

- Improve visibility

- Make strategy easier

Complexity rarely adds value.

You Can Withdraw Contributions (Sometimes!)

Here’s where people usually say: “Wait—what!?”

With a Roth IRA, you can withdraw your contributions at any time, for any reason, without taxes or penalties.

Why?

Because you already paid taxes on that money.

This makes Roth IRAs more flexible than many people think—but also more dangerous if misused.

Flexibility should be a backup plan, not a spending plan.

You Can Use IRA Money for Certain Life Events

Under specific rules, IRA funds may be accessed for:

- First-time home purchases

- Qualified education expenses

- Certain medical costs

These exceptions are tightly regulated and often misunderstood.

They reduce penalties—but may not eliminate taxes.

Knowing the rule is not enough.

Knowing the cost is what matters.

You Can Convert a Traditional IRA to a Roth IRA

This is one of the most powerful—and overlooked—IRA strategies.

A Roth conversion allows you to:

- Pay taxes now

- Lock in tax-free growth later

- Reduce future required distributions

This strategy is especially useful during:

- Lower-income years

- Market downturns

- Early retirement phases

Used wisely, conversions can dramatically improve long-term tax efficiency.

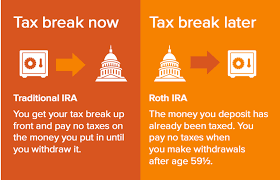

You Can Delay Taxes—or Eliminate Them

Traditional IRAs defer taxes.

Roth IRAs eliminate them (on qualified withdrawals).

This difference shapes:

- Retirement income strategy

- Tax planning flexibility

- Estate planning outcomes

Smart investors don’t ask, “Which IRA is better?”

They ask, “How do I use both strategically?”

You Can Also Mess This Up—Badly

IRAs are powerful, but the rules are strict.

Common costly mistakes include:

- Missing required distributions

- Withdrawing earnings too early

- Ignoring the five-year rules

- Triggering unnecessary taxes

- Treating IRAs like savings accounts

The IRS is patient—but not forgiving.

Why High Earners and Professionals Use IRAs Differently

For executives and business owners, IRAs are not just retirement tools.

They are tax-management tools.

They help with:

- Income smoothing

- Tax diversification

- Withdrawal sequencing

- Legacy planning

At higher income levels, strategy matters more than contribution size.

The CEO Mindset: An IRA Is a Long-Term Asset, Not a Piggy Bank

Successful decision-makers protect what compounds.

They understand:

- Tax-free money is rare

- Time is irreplaceable

- Small mistakes compound negatively

An IRA should be handled with the same care as a long-term business investment.

When Touching Your IRA Might Make Sense

There are moments when using IRA funds is reasonable:

- Severe financial emergencies

- Strategic tax planning

- Avoiding destructive high-interest debt

The key difference is intentionality.

Planned actions build wealth.

Emotional reactions destroy it.

Questions You Should Ask Before Doing Anything With Your IRA

Before moving, withdrawing, or converting, ask:

- Why am I doing this?

- What is the tax impact now and later?

- What future growth am I giving up?

- Is there a better alternative?

Good decisions age well.

Bad ones get expensive quietly.

Final Thoughts: Yes, Your IRA Is Powerful—If You Respect It

So yes—you can do more with your IRA than most people realize.

But just because you can doesn’t mean you should.

IRAs reward patience, planning, and discipline.

They punish impulse, confusion, and neglect.

Understand the rules.

Use the flexibility wisely.

And let your IRA do what it was designed to do—work quietly and powerfully for your future.

End of article.

Summary:

Use your IRA Funds to buy real estate using a self directed IRA.

Keywords:

IRA, self directed IRA, real estate, non-traditional investment

Article Body:

Copyright 2006 Damon Clifford

Everyone knows you can invest in stocks, bonds, and mutual funds with your IRA. About 97% of the trillions of dollars of IRA funds are invested in these types of assets. Did you know you can also invest your IRA funds into non-traditional assets like real estate, energy, and tax liens?

What!?

Yes, you can invest your IRA funds into a house, a duplex, or a commercial building along with many other non-traditional assets. A lot of people are choosing these types of investments to better diversify their retirement portfolio. These are the people that don�t want to see their portfolio rise and fall dramatically due to stock market fluctuations.

Any good broker will tell you to keep your portfolio diversified with many different stocks, bonds, and mutual funds. More savvy investors say to keep your portfolio diversified with many different assets such as stocks, bonds, mutual funds, energy & real estate. Some of their portfolio�s actually increased during the most recent bear market! This was due to their portfolio�s being truly diversified.

There are two main reasons that more and more people are choosing to invest a portion of their IRA funds in non-traditional assets. First, they don�t know or trust the stock market since it has performed poorly the last couple of years, and nobody can predict what the market will do over the next 5, 10, or 20 years. Second, they may or may not know what certain companies are doing on the other side of the country, but they do know about that �hot� piece of property just around the corner that would be a great rental house!

One of the added benefits to a self directed IRA is investing in assets that you know, and understand. The more you know and understand, the better judgment you can make in your own investments.

Once the self directed IRA is set up, you have investment control of the funds. You can use the funds to purchase the house and the income from rent will go back into your IRA. If you decide to sell the house, the capital gains from the sell will go back into your IRA as well. Depending on the type of IRA you have your gains can be either taxed deferred or tax free!

With the self directed IRA, you are in control. Many people are using the self directed IRA to take control of their retirement investments.

Stocks, bonds, and mutual funds still need to be in your portfolio to be diversified, but it�s important to understand that you do have choices outside the stock market!

Tinggalkan Balasan